Small Business Funding Ontario: Complete Guide to Small Business Financing in Ontario

If you’re looking for funding for small business in Ontario, you’re in the right place!

Because this is the ultimate, most comprehensive guide to small business funding for Ontario businesses.

We cover 47 distinct types of business funding in Ontario, comprising hundreds of government, non-profit, and private sector programs. These sources include money to start a new business (start-up funding), and money to operate and grow an existing business.

We’ve organized the types of funding into four categories:

Note: we use the term “financial incentive” throughout this guide. A financial incentive is a catchall term for any type of funding program available to business owners.

Here’s the complete list of types of small business funding for Ontario businesses:

Types of Funding for Ontario Businesses

| Self-Funding | Free Funding | Debt Financing | Equity Financing |

|---|---|---|---|

| Personal Savings | Grants | Government Loans/Credit | Accelerators |

| Personal Assets | Subsidies | Traditional Loans/Credit | Crowdfunding (Equity) |

| Side Hustles | Rebates | Asst-Backed Financing | Angel Investment |

| Bartering | Tax Credits | Revenue-Based Financing | Impact Investment |

| Crowdfunding (Rewards) | Pitch Competitions | Alternative Financing | Venture Capital |

| Bootstrapping | Incubators | Family Offices | |

| Crowdfunding (Donations) | Syndicate Investment | ||

| Sponsorships | Corporate Investment | ||

| Partnerships | Private Placement | ||

| Community Support |

I call this the “business funding universe” for Canadian entrepreneurs. Here’s a graphic to show how the types of funding are grouped:

Business Funding Universe: 47 Distinct Types of Funding for Entrepreneurs

In the sections that follow I cover all 47 types of funding, and I provide the following information on each:

- Description

- Pros & Cons

- When to Use It

But before I get into the types of funding, here’s an extremely important concept to understand:

Key Concept: “Stacking”

When you’re looking for funding for a business – whether it’s for a new startup or an existing business – remember that there are hundreds of funding programs available for Ontario entrepreneurs.

So instead of looking for only one program, you want to gather every program your business is eligible for and “stack” those programs. In some cases, it’s possible to pay for 100% of a business expense or asset by stacking multiple funding programs.

Now let’s get into the 47 types of funding!

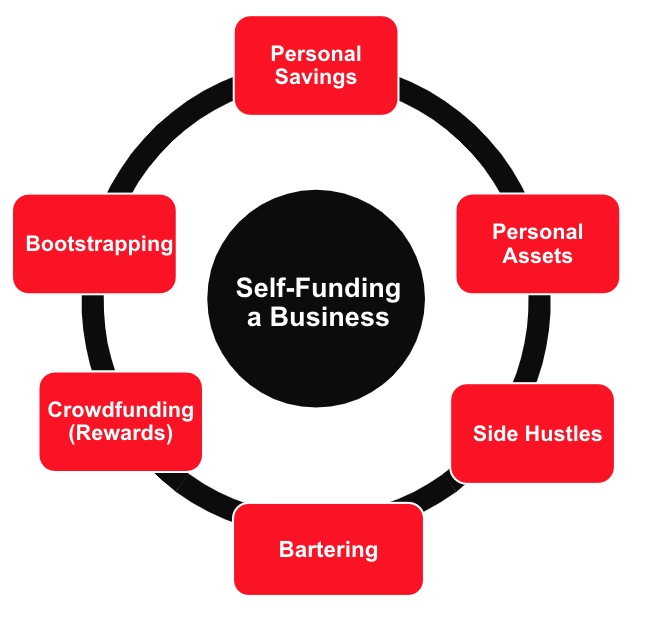

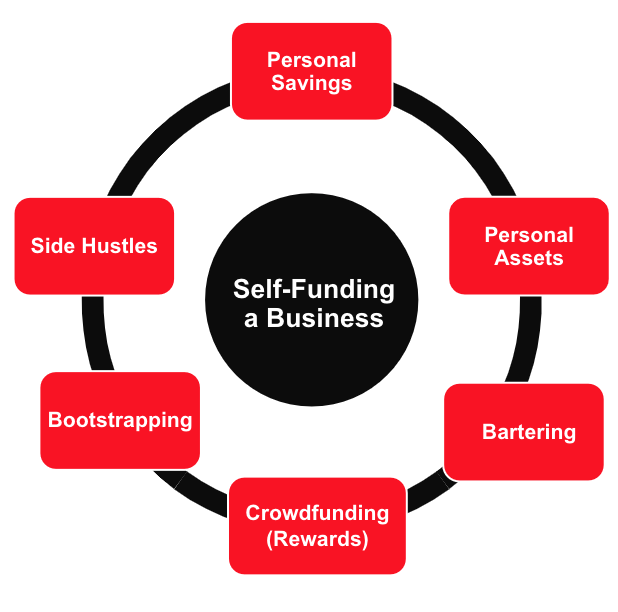

Self-Funding Your Canadian Business: 6 Strategies to Pay Your Own Way

When you’re starting out, your business is your baby, and you might decide to fund it yourself. This can mean tapping into your personal savings, considering the use of your retirement accounts, selling or leveraging personal assets, asking friends and family to chip in, or even starting a side hustle to drum up extra cash.

In the following sections we cover these 6 different types of self-funding that can be used for your business:

Personal Savings

Using your personal savings to fund your business is a straightforward approach. It’s like giving your business a loan from your own pocket. You won’t have to pay interest to a bank, but you’re taking on all the risk yourself.

Pros & Cons of Using Personal Savings for Your Business:

When to Use It: Use personal savings when you want to maintain complete control over your business and avoid debt, and when you have sufficient funds that won’t jeopardize your personal financial stability.

Personal Assets

Personal assets funding involves selling or leveraging valuable personal property, such as real estate, vehicles, or other significant possessions, to finance your business.

Pros & Cons of Using Personal Assets for Your Business:

When to Use It: Use personal assets when you need a large sum of capital quickly and are willing to risk or part with personal property to avoid taking on debt or outside investors.

Bartering

Bartering involves exchanging goods or services with another business or individual without the use of cash, allowing both parties to benefit from each other’s resources.

Pros & Cons of Using Bartering in Your Business:

When to Use It: Use bartering when you have valuable goods or services to offer and need to conserve cash while still acquiring necessary resources for your business.

Learn More About Bartering for BusinessSide Hustles

Side hustles involve doing additional jobs or freelance work alongside your primary business to earn extra income, which can be reinvested into your main venture.

Pros & Cons of Side Hustles (When Combined with Your Business):

When to Use It: Use side hustles when you need supplementary income to fund your business and can balance the additional workload without compromising the growth and management of your main business.

Explore the Best Side Hustles in OntarioCrowdfunding (Rewards)

Rewards crowdfunding involves raising small amounts of money from a large number of people through platforms like Kickstarter, offering backers non-monetary rewards such as products or services in return.

Pros & Cons of Using Rewards Crowdfunding for Your Business:

When to Use It: Use rewards crowdfunding when you have a marketable product or service and need to raise funds without taking on debt, while also seeking to build a loyal customer base and gain early market validation.

Learn More About Rewards Crowdfunding for BusinessBootstrapping

Bootstrapping involves funding your business through its own revenue streams without external financing.

For an online business, bootstrapping can involve selling products or services on social media, setting up an ecommerce website, and utilizing affiliate sales.

For an offline (i.e. in-person) business, this can involve doing local pop-ups and markets, selling your products through consignment in existing retail stores, or attending trade shows and expos.

Pros & Cons of Bootstrapping Your Business:

When to Use It: Use bootstrapping when you prefer to retain full control and ownership of your business and have a viable product or service that can generate revenue from the start.

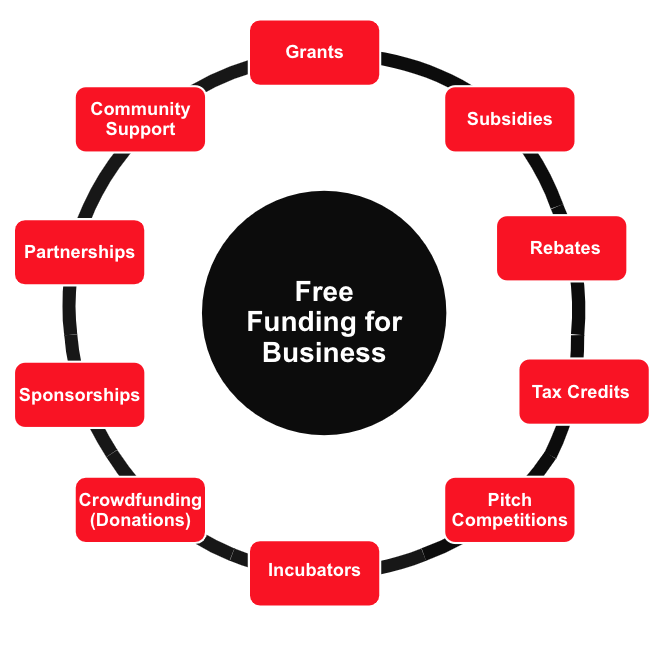

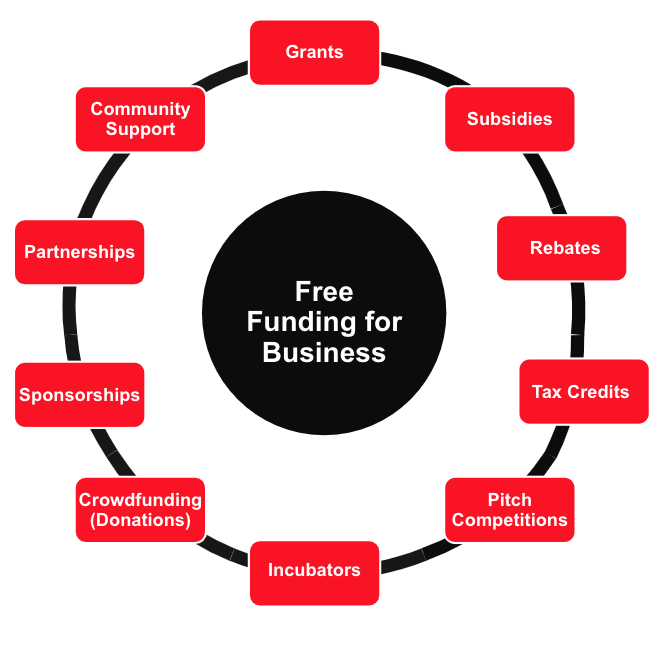

Learn More About Bootstrapping a BusinessFree Funding for Your Canadian Business: 10 Types of Free Money

To state the obvious: free money programs can offset your costs and help your business grow! And “free money” for businesses isn’t a myth – there are many programs and opportunities specifically designed to support small businesses in Canada.

Let’s get into these 10 free money programs:

Grants

Grants are non-repayable funds provided by government agencies, private organizations, or non-profits to support specific business activities or projects, such as research and development, innovation, exporting, and many other business activities.

Pros & Cons of Business Grants:

When to Use It: Use grants when you have a project or initiative that aligns with the funding organization’s goals, and you can meet the eligibility requirements and commit to the application and reporting process.

Learn More About Small Business Grants in OntarioSubsidies

Subsidies are financial assistance programs provided by the government to support specific business activities, such as wage support, employee training, export activities, or energy efficiency improvements.

Pros & Cons of Business Subsidies:

When to Use It: Use subsidies when you need to offset specific costs, such as wages, training, exporting, or implementing energy-efficient practices, and can comply with the associated regulations and reporting requirements.

Learn More About Wage Subsidies in OntarioRebates

Rebates are partial refunds provided to businesses after the purchase of specific goods or services, often aimed at encouraging investment in particular areas, such as energy efficiency, technology adoption, or environmental sustainability.

Pros & Cons of Business Rebates:

When to Use It: Use rebates when making investments in areas eligible for rebate programs, such as energy-efficient equipment or environmentally friendly technologies, and when you can afford the initial expenditure and navigate the rebate application process.

Learn More About Business Rebates in OntarioTax Credits

Tax credits are financial benefits provided by the government that directly reduce the amount of taxes owed.

Pros & Cons of Business Tax Credits:

When to Use It: Use tax credits when you are undertaking eligible activities like research and development, capital investments, or environmentally sustainable projects, and can ensure proper documentation and compliance with tax regulations.

Learn About Business Tax Credits in OntarioPitch Competitions

Pitch competitions are events where entrepreneurs present their business ideas to a panel of judges, often comprising investors or industry experts, for a chance to win funding, mentorship, or other resources.

Pros & Cons of Pitch Competitions:

When to Use It: Use pitch competitions when you have a well-developed business idea or product and are looking for funding, exposure, or mentorship. They are particularly beneficial if you’re confident in your ability to present and defend your business concept in front of an audience and panel.

Learn More About Pitch Competitions in OntarioIncubators

A business incubator is a program designed to support early-stage startups by providing resources such as office space, mentorship, networking opportunities, and sometimes funding, to help them grow and succeed.

Pros & Cons of Business Incubators:

When to Use It: Use a business incubator when you are an early-stage startup needing guidance, resources, and a supportive environment to develop your business idea, especially if you lack initial capital or industry connections.

Learn More About Business IncubatorsCrowdfunding (Donations)

Donations crowdfunding involves raising funds from a large number of people, typically via online platforms like GoFundMe, where backers contribute without expecting any financial return. This approach is often used for businesses with a strong community or social impact focus.

Pros & Cons of Donations Crowdfunding for Business:

When to Use It: Use donations crowdfunding when your business has a strong social or community aspect that resonates with potential donors, and when you’re able to create a compelling narrative to engage supporters. It’s particularly useful for early-stage businesses or projects that may not yet be attractive to traditional investors.

Learn More About Donations Crowdfunding for BusinessSponsorships

Sponsorships involve partnering with other businesses or organizations that provide financial or in-kind support in exchange for promotional opportunities, brand visibility, or other benefits.

Pros & Cons of Business Sponsorships:

When to Use It: Use sponsorships when your business can offer visibility or marketing benefits to sponsors, such as events, media coverage, or audience access, and when you’re looking for funding or resources without taking on debt or giving up equity. It’s particularly effective for businesses in industries like sports, entertainment, or community events.

Learn More About Business SponsorshipsPartnerships

Partnerships involve collaborating with other businesses or individuals to share resources, expertise, or market access for mutual benefit. These can take the form of formal joint ventures or informal collaborations.

Pros & Cons of Business Partnerships:

When to Use It: Use partnerships when your business can benefit from the complementary strengths of another entity, such as entering new markets, sharing costs for large projects, or enhancing your product or service offerings. It’s ideal when both parties have clearly defined roles and a shared vision for the partnership’s goals.

Learn More About Business PartnershipsCommunity Support (In-Kind)

In-kind community support involves receiving non-monetary assistance from local supporters, businesses, or organizations. This can include donated goods, services, volunteer time, or expertise.

There are four organizations that provide significant in-kind support to businesses in Ontario: are Business Improvement Areas (BIAs) and Chambers of Commerce.

- Business Improvement Areas (BIAs)

- Chambers of Commerce

- Small Business Enterprise Centres (SBECs)

- Community Futures Development Corporations (CFDCs)

Pros & Cons of In-Kind Community Support for Business:

When to Use It: Use community support in-kind when you’re looking to reduce costs and build strong ties with the local community, especially for businesses with a community or social impact focus. It’s particularly useful for startups or small businesses that may not have the budget for certain resources or services.

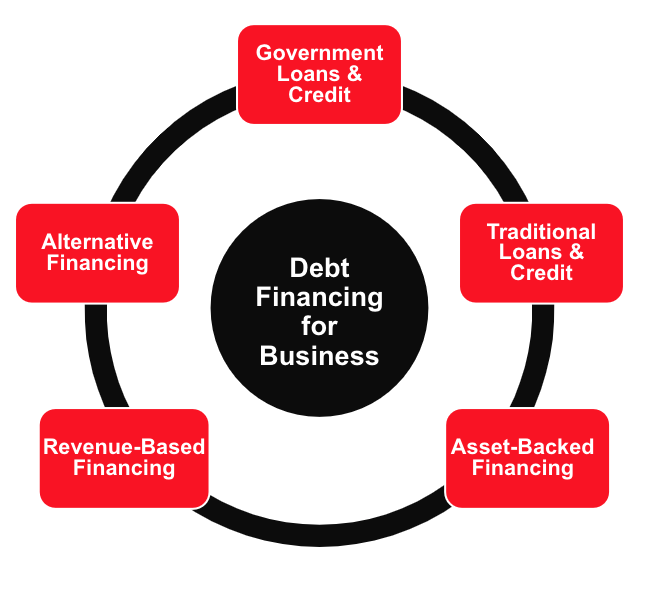

Learn More About Business Improvements Areas (BIAs), Chambers of Commerce, Small Business Enterprise Centres, and Community Futures Development CorporationsDebt Financing for Your Canadian Business: 22 Types of Loans & Credit

When you’re looking for money to grow your business, debt financing can be a viable route. It’s all about borrowing funds and paying them back over time, usually with interest. Think of it as getting a loan that you’ll budget for and repay as your business earns.

We’ve identified 22 types of debt financing for Canadian businesses. To understand them better, we’ve grouped them into 5 sub-categories:

- Government Loan & Credit Programs

- Traditional (Bank) Loan & Credit Products

- Asset-Backed Financing

- Revenue-Based Financing

- Alternative Financing

In the sections below we cover each of the 5 sub-categories, along with the types of debt financing that fall into each:

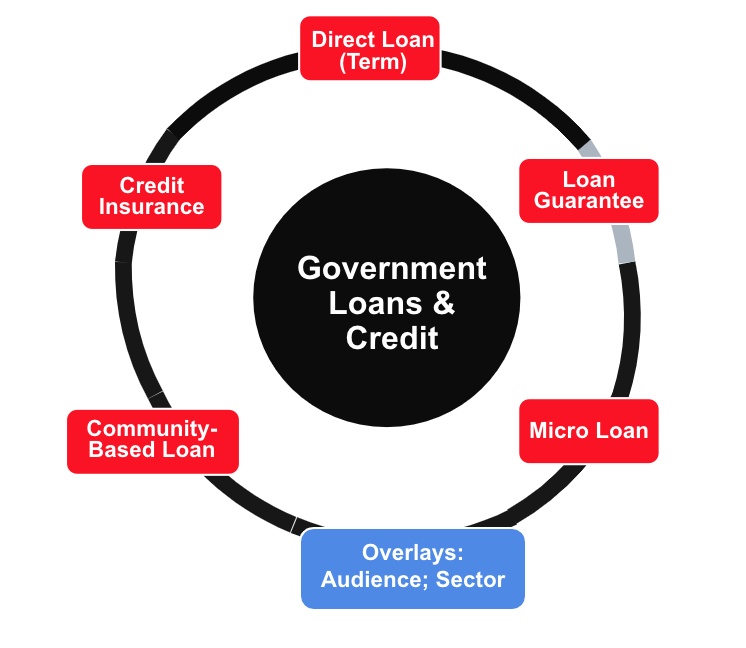

Government Loan & Credit Programs

Government loan and credit programs…

We’ve identified 5 types of government loan and credit programs for Ontario entrepreneurs, and cover each below:

Direct Government Loan (Term)

Direct government business loans are funds provided straight from federal or provincial government agencies such as BDC (Business Development Bank of Canada), EDC (Export Development Canada), or FCC (Farm Credit Canada). These loans support Canadian businesses with financing for growth, equipment, exports, working capital, and sector-specific needs..

Pros & Cons of Direct Government Loans for Business:

When to Use It: Use direct government loans when you’re looking for patient capital to support growth, innovation, or expansion, especially if you’re in sectors like manufacturing, exporting, or agriculture. They’re ideal for businesses that may not meet commercial bank criteria but have a strong business plan and need strategic, long-term support.

Learn More About Using Government Term Loans for Ontario BusinessGovernment-Guaranteed Loan

A government-guaranteed loan is a loan in which the government promises to repay a portion or the entirety of the loan if the borrower defaults. These loans are often provided through financial institutions and are designed to help businesses access funding with more favourable terms.

Pros & Cons of Government-Guaranteed Loans for Business:

When to Use It: Use a government-guaranteed loan when your business needs funding but may not qualify for traditional loans due to limited credit history or other factors. It’s ideal for businesses looking to expand, purchase equipment, or manage cash flow, especially in sectors that the government wants to support or stimulate.

Learn About Government-Guaranteed Loans for Ontario BusinessMicro Loan

Government micro loans are small loans—typically under $50,000—provided directly by government agencies or through non-profit partners to help startups, small businesses, and underrepresented entrepreneurs access early-stage capital. In Canada, programs like those from Futurpreneur Canada, Community Futures, and BDC offer this type of support.

Pros & Cons of Government Micro Loans for Business:

When to Use It: Use a government micro loan when you’re launching or growing a small business and need modest capital for things like inventory, equipment, or marketing. It’s especially useful for first-time entrepreneurs, rural businesses, or those from equity-deserving communities who need funding plus hands-on support.

Learn About Government Micro Loans for BusinessCommunity-Based Loan (Government-Supported)

Government community-based loans are small business loans provided by federally funded, locally managed organizations such as Community Futures. These loans are designed to support rural and regional economic development by offering accessible financing to local entrepreneurs who may not qualify for traditional loans.

Pros & Cons of Government Community-Based Loans for Business:

When to Use It: Use a community-based loan when you’re starting or growing a business in a rural or underserved area and need financing from a lender that understands local economic conditions. It’s ideal for entrepreneurs who need both funding and hands-on business development support in their community.

Learn About Government Community-Based Loans for BusinessCredit Insurance

Government credit insurance, primarily offered in Canada through Export Development Canada (EDC), protects businesses against the risk of non-payment by customers—especially in international trade. It ensures that if a buyer defaults due to bankruptcy, political instability, or other covered reasons, the business still gets paid.

Pros & Cons of Government Credit Insurance for Business:

When to Use It: Use credit insurance when extending payment terms to customers—particularly international ones—and you want to reduce the risk of financial loss from defaults. It’s ideal for exporters, manufacturers, or any business with large accounts receivable and exposure to customer payment risk.

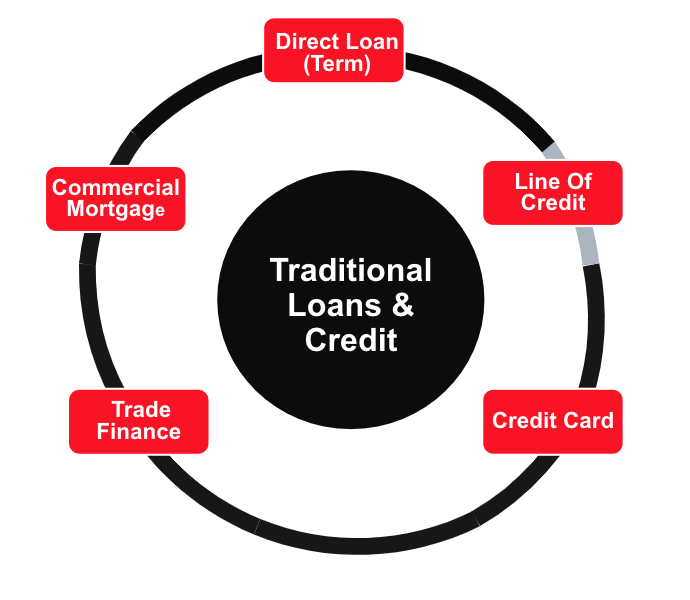

Learn About Government Credit Insurance for BusinessTraditional (Bank) Loan & Credit Products

When most business owners think of debt financing, this is often what they have in mind: the conventional loans and credit products offered by banks and credit unions.

We’ve identified 4 types of traditional loans and credit products for Canadian entrepreneurs, and cover each below:

Direct Loan (Term)

A term loan is a lump sum of money borrowed from a lender that is repaid over a fixed period with regular payments, including interest. It’s typically used for significant investments like equipment purchases, expansion, or other capital expenditures.

Pros & Cons of Term Loans for Business:

When to Use It: Use a term loan when you need a large amount of capital for specific long-term investments and have a clear plan for generating the revenue needed to repay the loan. It’s suitable for established businesses with strong credit and predictable cash flow.

Learn More About Using Traditional Term Loans for BusinessBusiness Line of Credit

A business line of credit is a flexible financing option that provides access to a predetermined amount of funds, which a business can draw from as needed. Interest is only charged on the amount borrowed, not the entire credit limit, and funds can be reused as they are repaid.

Pros & Cons of Business Lines of Credit:

When to Use It: Use a business line of credit when you need flexible, short-term funding to manage cash flow, cover operational expenses, or take advantage of unexpected opportunities. It’s ideal for businesses with fluctuating capital needs and those that can manage regular repayments.

Learn More About Business Lines of CreditBusiness Credit Card

A business credit card provides a revolving line of credit that can be used to cover day-to-day business expenses, similar to a personal credit card. It offers convenience for managing expenses and often includes rewards programs or cashback offers tailored to business needs.

Pros & Cons of Business Credit Cards:

When to Use It: Use a business credit card for short-term financing of daily expenses, such as office supplies, travel, or minor equipment purchases, especially if you can pay off the balance each month to avoid interest charges. It’s also useful for tracking and managing business expenses and building credit.

Learn More About Business Credit CardsTrade Finance

Trade finance includes a range of financial products and services designed to facilitate international and domestic trade. It includes instruments like letters of credit, export credit, and factoring, which help manage the risks and provide the necessary capital for buying and selling goods and services across borders.

Pros & Cons of Trade Finance:

When to Use It: Use trade finance when engaging in international trade to ensure smooth transactions and manage risks associated with cross-border commerce, such as currency fluctuations, non-payment, or geopolitical issues. It’s particularly useful for businesses looking to expand into new markets or requiring capital to fulfill large orders.

Learn More About Trade FinanceCommercial Mortgage

A commercial mortgage is a loan secured by commercial property, such as an office building, warehouse, or retail space, used to purchase, refinance, or redevelop the property.

Pros & Cons of Commercial Mortgages:

When to Use It: Use a commercial mortgage when you need to purchase or refinance commercial real estate and have the financial stability to handle the long-term commitment. It’s suitable for businesses looking to expand their physical presence or invest in property as part of their growth strategy.

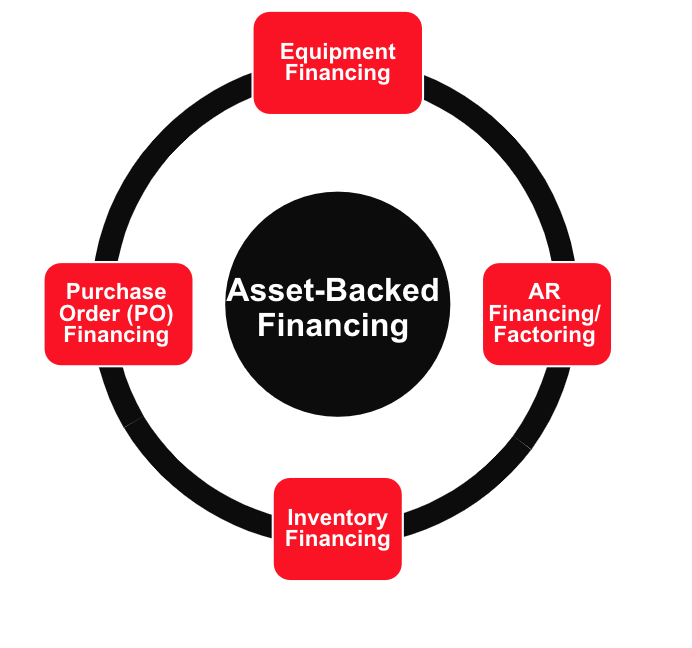

Learn More About Commercial MortgagesAsset-Backed Financing

Asset-backed financing means you’re borrowing against the value of your company’s assets. Your equipment, inventory, or property can secure your loan, potentially getting you more capital based on their worth.

The four main types of asset-backed financing are the following:

Equipment Financing

Equipment financing involves obtaining a loan or lease to purchase business-related equipment, such as machinery, vehicles, or technology. The equipment itself often serves as collateral for the loan.

Pros & Cons of Equipment Financing:

When to Use It: Use equipment financing when you need to acquire expensive equipment crucial for business operations but prefer to preserve cash flow by spreading the payments over time. It’s ideal for businesses requiring significant machinery, technology, or vehicles to grow and operate efficiently.

Learn More About Equipment FinancingAccounts Receivable (AR) Factoring and Financing

Accounts receivable (AR) factoring and financing (also called invoice factoring and financing) are two ways to use your outstanding customer invoices to generate cash.

Accounts receivable financing allows a business to borrow money against its outstanding invoices. The business retains ownership of the invoices and is responsible for collecting payments from customers, repaying the lender as the invoices are paid.

Pros & Cons of Accounts Receivable Financing:

When to Use It: Use accounts receivable financing when you need short-term funding to cover operational costs but want to maintain control over your billing and collections. It’s ideal for businesses with reliable customers and predictable invoice payments but slow cash conversion cycles.

Accounts receivable factoring involves selling your outstanding invoices at a discount to a factoring company. The company pays you a percentage of the invoice amount upfront and takes responsibility for collecting the full invoice amount from the customer.

Pros & Cons of Accounts Receivable Factoring:

When to Use It: Use accounts receivable factoring when you need immediate working capital and have reliable customers but can’t wait for standard payment terms. It’s especially useful for businesses with long invoice cycles or limited access to traditional financing.

Learn More About AR Factoring or Accounts Receivable FinancingInventory Financing

Inventory financing is a type of short-term loan or line of credit used to purchase inventory. The inventory itself often serves as collateral for the loan, enabling businesses to buy stock without immediately depleting cash reserves.

Pros & Cons of Inventory Financing:

When to Use It: Use inventory financing when you need to purchase large quantities of inventory to prepare for high-demand periods or seasonal sales, and when maintaining cash flow is essential. It’s particularly useful for retail and wholesale businesses that need to keep shelves stocked but prefer to avoid upfront costs.

Learn More About Inventory FinancingPurchase Order (PO) Financing

Purchase order (PO) financing provides short-term funding to help businesses pay suppliers for goods needed to fulfill large customer orders. The financing company pays the supplier directly, and is repaid once the customer receives the order and makes payment.

Pros & Cons of Using Purchase Order (PO) Financing for Your Business:

When to Use It: Use PO financing when you receive a large customer order but lack the cash to cover production or inventory costs. It’s ideal for wholesalers, manufacturers, or importers that need to bridge the gap between receiving an order and getting paid.

Learn More About Purchase Order (PO) Financing for BusinessRevenue-Based Financing

With revenue-based financing, you borrow against future revenues, paying back a percentage of your sales. This is less about collateral and more about cash flow—a good fit if your sales are solid but unpredictable.

The four main types of revenue-based financing are:

Merchant Cash Advance

A merchant cash advance (MCA) provides businesses with a lump sum of cash in exchange for a percentage of future credit card sales. Repayments are typically made daily or weekly based on sales volume.

Pros & Cons of Merchant Cash Advance:

When to Use It: Use a merchant cash advance when you need fast funding for short-term expenses, emergencies, or opportunities and have a consistent volume of credit card sales to manage flexible repayments. It’s suitable for businesses that may not qualify for traditional loans but need immediate working capital.

Learn More About Merchant Cash AdvanceTax Credit Financing

Tax credit financing involves obtaining a loan or line of credit against future tax credits your business expects to receive, such as Scientific Research and Experimental Development (SR&ED) credits or film production tax credits.

Pros & Cons of Tax Credit Financing:

When to Use It: Use tax credit financing when your business has earned or expects to earn significant tax credits and needs immediate capital for ongoing operations or new projects. It’s suitable for businesses in industries like research and development or film production, where tax credits are substantial but disbursements are delayed.

Learn More About Tax Credit FinancingSupply Chain Financing

Supply chain financing, also known as reverse factoring, is a financial arrangement where a buyer works with a financial institution to allow its suppliers to receive early payment on their invoices—typically at a lower cost due to the buyer’s stronger credit profile. The buyer pays the financer later, on the original due date.

Pros & Cons of Supply Chain Financing:

When to Use It: Use supply chain financing when you’re a buyer with strong credit looking to support your suppliers and optimize working capital. It’s also valuable for suppliers working with large buyers who offer this program, as it provides faster access to cash at a lower financing cost.

Learn More About Supply Chain FinancingRoyalty Financing

Royalty financing provides capital to a business in exchange for a percentage of future revenues, typically until a predetermined return is paid back. Unlike equity financing, the investor doesn’t take ownership, and unlike a loan, repayments are tied to business performance.

Pros & Cons of Royalty Financing:

When to Use It: Use royalty financing when you want to retain full ownership of your business, expect consistent revenue, and prefer performance-based repayments over fixed loan schedules. It’s particularly suitable for businesses with strong margins and predictable sales, such as consumer products or subscription services.

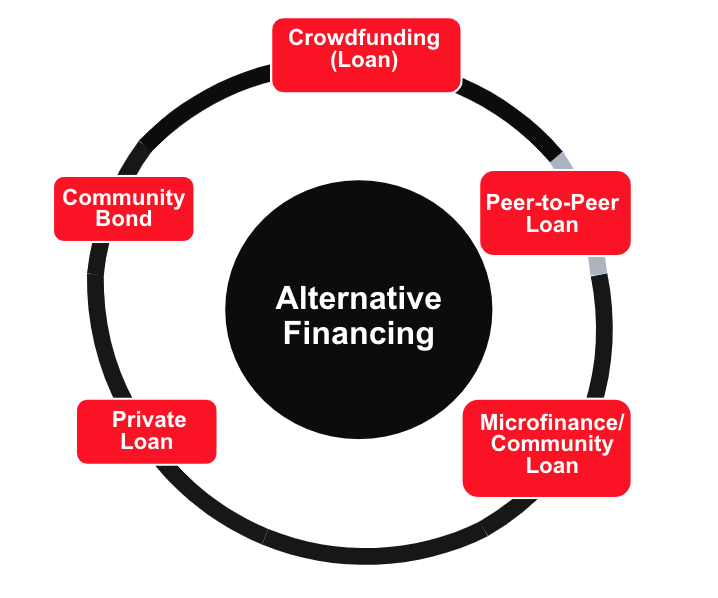

Learn More About Royalty FinancingAlternative Financing

Alternative financing for is a category that is growing in popularity for Canadian businesses (and I personally think crowdfunding is an area that has huge potential and will grow in coming years). This type of financing is a good option when you’re seeking flexibility or when conventional banks aren’t an option.

There are 5 main types of alternative debt financing:

Crowdfunding (Debt/Loan)

Debt crowdfunding involves raising funds from a large number of individual investors through online platforms. Businesses receive a loan and repay it with interest over time, similar to traditional loans but funded by multiple investors.

Pros & Cons of Debt Crowdfunding for Business:

When to Use It: Use debt crowdfunding when you need to raise funds quickly and may not qualify for traditional bank loans, especially if you can leverage a strong network or community of supporters. It’s suitable for businesses that can attract individual investors with a compelling story and clear repayment plan.

Learn More About Debt/Loan Crowdfunding for BusinessPeer-to-Peer Loan

Peer-to-peer (P2P) loans are obtained through online platforms that connect businesses directly with individual lenders. These loans typically offer a range of terms and interest rates, depending on the business’s creditworthiness and the lender’s criteria.

Pros & Cons of Peer-to-Peer Loans for Business:

When to Use It: Use peer-to-peer loans when you need quick access to capital and have a reasonably good credit score, but prefer a more flexible and accessible option than traditional bank loans. It’s suitable for small to medium-sized businesses looking for alternative financing solutions.

Learn More About Peer-to-Peer Loans for BusinessMicrofinance/Community Loan (Private & Non-Profit)

Microfinance/community loans are small loans offered by non-profit organizations, community lenders, or mission-driven private institutions to help underserved entrepreneurs and small businesses access capital. These lenders often focus on inclusion, supporting women, newcomers, Indigenous entrepreneurs, or those with limited credit history.

Pros & Cons of Microfinance/Community Loans for Business:

When to Use It: Use private/non-profit sector microfinance or community loans when you’re starting or growing a small business and need modest capital but face barriers accessing traditional financing. These loans are especially valuable for entrepreneurs in marginalized communities or those needing both funding and support.

Learn More About Microfinance/Community Loans for BusinessPrivate Loan

Private loans for business include funds provided by family, friends, and private lenders (such as wealthy individuals) or through private loan brokers. These loans offer more personalized and flexible terms compared to traditional banking systems

Pros & Cons of Private Loans for Business:

When to Use It: Use private loans when you need quick and flexible financing, especially if you do not qualify for traditional bank loans or need customized terms. They are ideal for businesses looking for alternative funding options and willing to manage personal dynamics and potentially higher costs.

Learn More About Private Loans for BusinessCommunity Bond

A community bond is an investment tool that allows businesses—typically social enterprises or community-focused ventures—to raise capital from local supporters. Investors purchase the bond, and the business repays it over time with interest, similar to a traditional loan but with a community-driven focus.

Pros & Cons of Community Bonds for Business:

When to Use It: Use a community bond when your business has a strong local or social impact and you want to raise capital from people who care about your mission. It’s ideal for cooperatives, nonprofits with revenue-generating activities, and socially minded small businesses looking to finance a specific project or expansion.

Learn More About Community Bonds for BusinessEquity Financing for Your Canadian Business: 9 Ways to Sell a Stake in Your Business

Equity financing invites investors to fund your company in exchange for a piece of ownership. This can be a pivotal step in your business growth, offering capital while avoiding debt.

There are 9 main types of equity financing that entrepreneurs can access in Canada, which we cover below:

Accelerator

A business accelerator that provides equity investment offers startups intensive, short-term support and funding in exchange for an ownership stake. These programs typically include mentorship, networking opportunities, and resources designed to rapidly scale the business.

Pros & Cons of Business Accelerators:

When to Use It: Use a business accelerator for equity investment when you have a validated business model and are ready to scale quickly, seeking both financial investment and expert guidance. It’s ideal for startups looking to grow rapidly and gain access to a robust network of mentors, investors, and industry connections.

Learn the Top 10 Business Accelerators in OntarioCrowdfunding (Equity)

Equity crowdfunding involves raising capital from a large number of investors through online platforms in exchange for shares in the company. This method allows businesses to access funds from both accredited and non-accredited investors who gain equity ownership.

Pros & Cons of Equity Crowdfunding:

When to Use It: Use equity crowdfunding when you have a compelling business idea or product and need to raise capital from a broad audience. It’s suitable for startups and growing businesses looking to build a large community of investors and gain substantial funding without relying solely on traditional venture capital.

Learn More About Equity CrowdfundingAngel Investment

Angel investment involves receiving capital from wealthy individuals, known as angel investors, who provide funding in exchange for equity ownership in the business. These investors often bring valuable expertise and mentorship along with their financial support.

Pros & Cons of Angel Investment:

When to Use It: Use angel investment when you need substantial capital to grow your business and can benefit from the investor’s experience and network. It’s suitable for early-stage startups with high growth potential that are willing to exchange equity for both financial support and strategic guidance.

Learn More About Angel InvestmentImpact Investment

Impact investment involves receiving funding from investors who seek both financial returns and positive social or environmental impact. These investors prioritize businesses that address significant societal challenges while maintaining profitability.

Pros & Cons of Impact Investment:

When to Use It: Use impact investment when your business aims to address social or environmental issues and you need capital to scale these efforts while maintaining financial sustainability. It’s ideal for businesses committed to making a positive impact and attracting investors aligned with their mission.

Learn More About Impact InvestmentVenture Capital

Venture capital (VC) involves receiving funding from professional investment firms that specialize in high-risk, high-reward startups. In exchange for significant capital, these firms receive equity stakes in the business and often play an active role in its strategic direction.

Pros & Cons of Venture Capital:

When to Use It: Use venture capital when your business has high growth potential and you need substantial funding to scale rapidly. It’s suitable for startups in technology or innovative sectors that require large capital investments and can benefit from strategic partnerships and expertise from experienced investors.

Learn More About Venture CapitalFamily Office Investment

Family office investment involves securing funding from family offices, which are private wealth management firms that handle the investments and financial affairs of affluent families. These investments can offer flexible terms and substantial capital, often with a long-term perspective.

Pros & Cons of Family Office Investment:

When to Use It: Use family office investment when you need substantial funding and prefer a long-term investment perspective with flexible terms. It’s suitable for businesses that can benefit from strategic support and patient capital, particularly in industries that align with the family office’s interests and values.

Learn More About Family Office InvestmentSyndicate Investment

Syndicate investment is a type of equity financing where a lead investor pools capital from a group of co-investors (the syndicate) to invest in a single business. The lead investor typically conducts due diligence, negotiates terms, and manages the relationship with the business on behalf of the group.

Pros & Cons of Syndicate Investment:

When to Use It: Use syndicate investment when you’re raising a substantial funding round and want the credibility and strategic value of a lead investor, along with access to multiple co-investors. It’s especially suitable for startups seeking capital from angel networks or platforms like AngelList, where syndicate investing is common.

Learn More About Syndicate InvestmentStrategic Corporate Investment

Strategic corporate investment involves receiving funding from established companies that are looking to invest in startups or smaller businesses that complement their own operations. These investments can include capital, resources, and expertise, often with the intent of forming a strategic partnership.

Pros & Cons of Strategic Corporate Investment:

When to Use It: Use strategic corporate investment when your business can benefit from the resources, expertise, and market position of a larger corporate partner, and when there is a clear alignment of strategic goals. It’s suitable for businesses looking to scale rapidly and willing to collaborate closely with an established company in their industry.

Learn More About Strategic Corporate InvestmentPrivate Placement

Private placement is a method of raising capital by selling equity or debt securities directly to a select group of investors—such as accredited individuals, institutional investors, or private funds—rather than through a public offering.

Pros & Cons of Private Placement:

When to Use It: Use private placement when your business is ready to raise a sizable round of funding from sophisticated investors but wants to avoid the complexity and cost of going public. It’s ideal for growth-stage companies looking for strategic capital with more flexibility than traditional public markets allow.

Learn More About Private Placement